What is a Reverse Mortgage?

A Reverse Mortgage is a home loan available to homeowners over 55. That does not require regular repayment. Your borrowing capacity is determined by your age, so at 55 years old a borrower can borrow up to 15% of the total value of their property. This amount you can borrow goes up by 1 percent every year so by age 90 a borrower could borrow up to 50% of the property value. The borrower maintains ownership of the home.

A Reverse Mortgage does not need to be paid back until the last borrower leaves the security property permanently. This can be because of a sale, going into aged care or death. The loan comes with a lifetime occupancy guarantee. The lender cannot ask for any repayments for the life of the loan. However, if you do wish to make repayments you are free to do so.

A Reverse Mortgage can be used in many ways including- consolidating debts such as paying off a mortgage or credit cards, helping family, new motor vehicles, renovations, holidays, strata levies, aged care costs, or simply to supplement income and covering living expenses.

Reverse Mortgages are the most heavily regulated financial loan product in Australia. They come with a no negative equity guarantee so you can never owe more than the value of the property they are also subject to ASIC’s best interest duty.

Reverse mortgages are a great financial tool for older Australians to achieve their long and short term financial aspirations, but over the years there have been some negative myths about the products which are untrue. We are now going to go through these myths and dispel them.

With a Reverse Mortgage you can lose your home?

No, with a Reverse mortgage, the borrowers retain ownership of their home. They receive guaranteed lifetime occupancy. The lender can never ask for a repayment until all borrowers have permanently left the home. This means that the borrowers can remain in their homes as long as they want.

Will I leave my children in debt?

With a Reverse mortgage you can never leave your children a debt that cannot be paid by the sale of the security property. This is because there is a non-negative equity guarantee. No matter how big the loan balance is they can only ever request a repayment up to the value of the property.

Will I be able to leave an inheritance?

Yes, a Reverse Mortgage is usually only a small part of the value of the property. Any remaining equity in the property goes to the beneficiaries. The property can also be paid back by any means and does not need to be sold. A beneficiary can refinance to an ordinary mortgage. In many cases when used appropriately, a reverse mortgage can ensure you leave your children a bigger inheritance. The below is a true story.

Mavis (aged 87) and Angus (aged 85) have lived in their home in the Hills District for over 60 years.

They have a reverse mortgage that has a balance of approximately $490,000. They first took out a reverse mortgage in 2007. Then their property was only worth around $700,000. They could either sell and purchase in a retirement village for $500,000 and have some savings in the bank after paying agent fees and stamp duty. Instead, they took out a reverse mortgage and have enjoyed their property and used funds to enhance their retirement all whilst the equity in their home has increased. They have drawn a few lump sums and $1000 dollars per month since 2007. In late 2023 their property was valued at 2.5 million. Their family has assets with 2 million dollars of equity in it rather than a retirement village home of less than half a million.

I will be charged interest on the whole loan balance?

No, with a reverse mortgage, you are only charged interest on what you use. So if you do not draw down you are not charged interest.

Are Reverse Mortgages a safe and ethical product?

Reverse Mortgages are extremely safe products and are the most heavily regulated financial products on the Australian market. Borrowers are protected by a non-negative equity guarantee which means you can never owe more than the value of the property. Borrowers are also protected by a best interest duty. This means that lenders and brokers must be able to prove to regulators that a Reverse Mortgage is in the client’s best interest otherwise they cannot do the loan.

All lenders conduct compliance calls to ensure the borrower understands what they are doing and to make sure there is no elder abuse or exploitation of the borrower. Furthermore, all borrowers must get independent legal advice upon signing their Reverse Mortgage services contract.

Ultimately, Reverse Mortgages provide freedom to maintain one’s current lifestyle and to fulfill one’s aspirations. ASIC’s reverse mortgage consumer survey found 29 out of 30 borrowers recommended a reverse mortgage.

Bank of Mum and Dad & Reverse Mortgage a Tool for Intergenerational Wealth

Reverse Mortgage and Age Pension Entitlement

Other blog posts

-

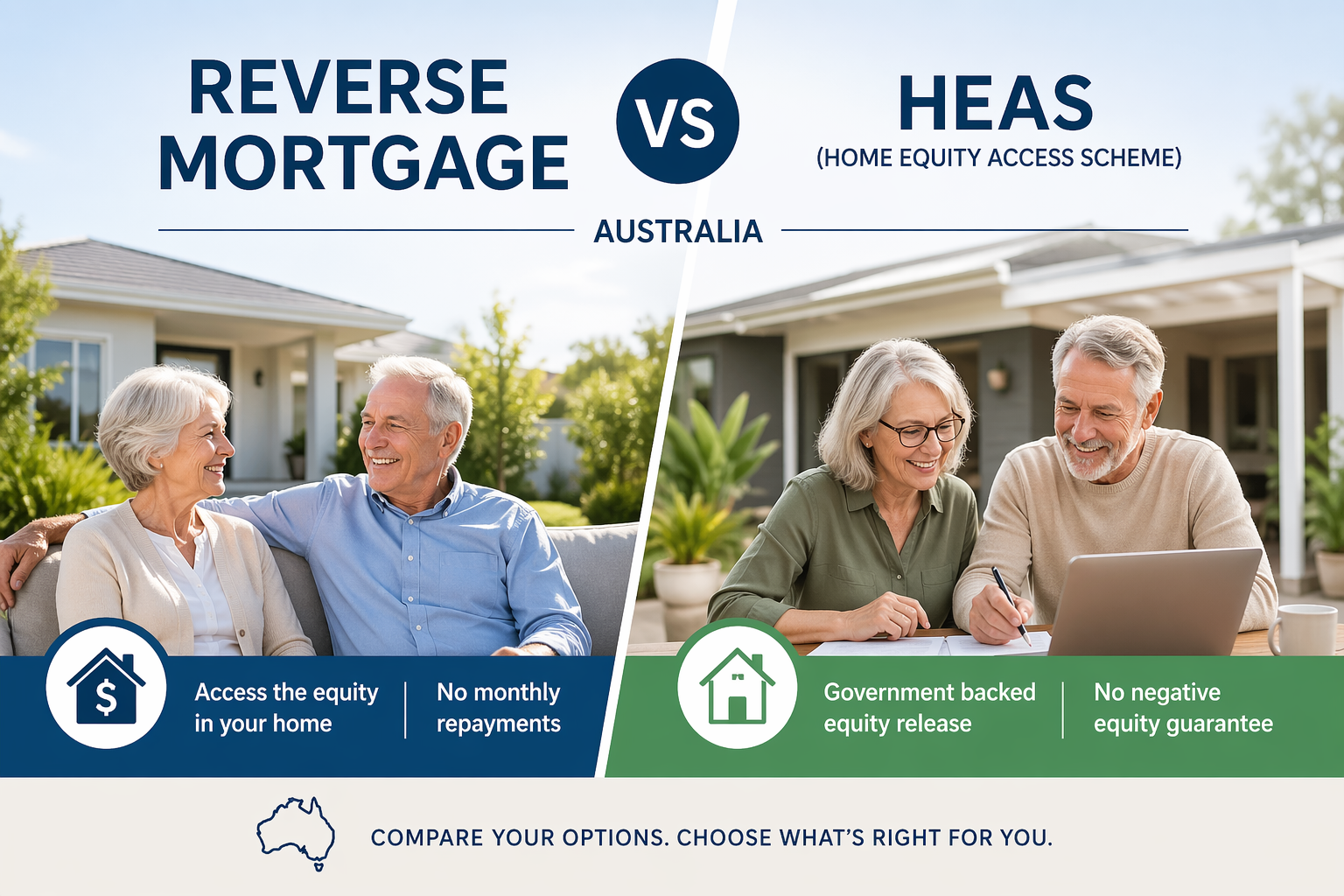

Reverse Mortgage vs Home Equity Access Scheme: What’s Better in 2026?

As more Australians enter retirement with valuable property but limited cash flow, the need to access home equity has grown significantly. In 2026, two of the most popular options are: Reverse mortgages (private lenders) The Home Equity Access Scheme (HEAS) (Australian Government) Both allow you to unlock the value in...... -

Energy Rebates for Australian Seniors in 2025–26

With rising energy costs across Australia, many seniors are looking for ways to manage household expenses more effectively. In response, both federal and state governments—particularly in NSW—are offering a range of support measures designed to reduce energy bills. The energy rebates for Australian seniors in 2025–26 are an important form...... -

Comparing Reverse Mortgage Providers and Products in Australia (2026)

Reverse mortgages are becoming an increasingly popular option for older Australians who want to unlock the value of their homes without selling. As property values increase and retirement funding needs evolve, many homeowners are exploring reverse mortgage finance solutions to supplement income or fund lifestyle expenses....